In addition to the West Coast’s import container records, other major port regions posted positive year-over-year gains in March based on data from the PIERS database:

- Pacific Northwest (which includes Tacoma, Seattle and Everett ports): Up 67%

- British Columbia (Prince Rupert): Up 55%

- Gulf Coast ports (Houston, Mobile and New Orleans): Up 37%

- East Coast ports: Up 40%

Find loads and trucks on the largest load board network in North America.

The top four port markets ranked by loaded import container volume (New York, Savannah, Los Angeles and Long Beach) accounted for 60% of total monthly volume in March and reported a 68% y/y increase in volume.

For carriers and brokers in these port markets, DAT load posts track closely with import container volumes. So as port congestion continues to impact port throughput on higher y/y volumes, market participants can expect a continuation of current market volatility and tight capacity well into the summer.

All rates exclude fuel unless otherwise noted.

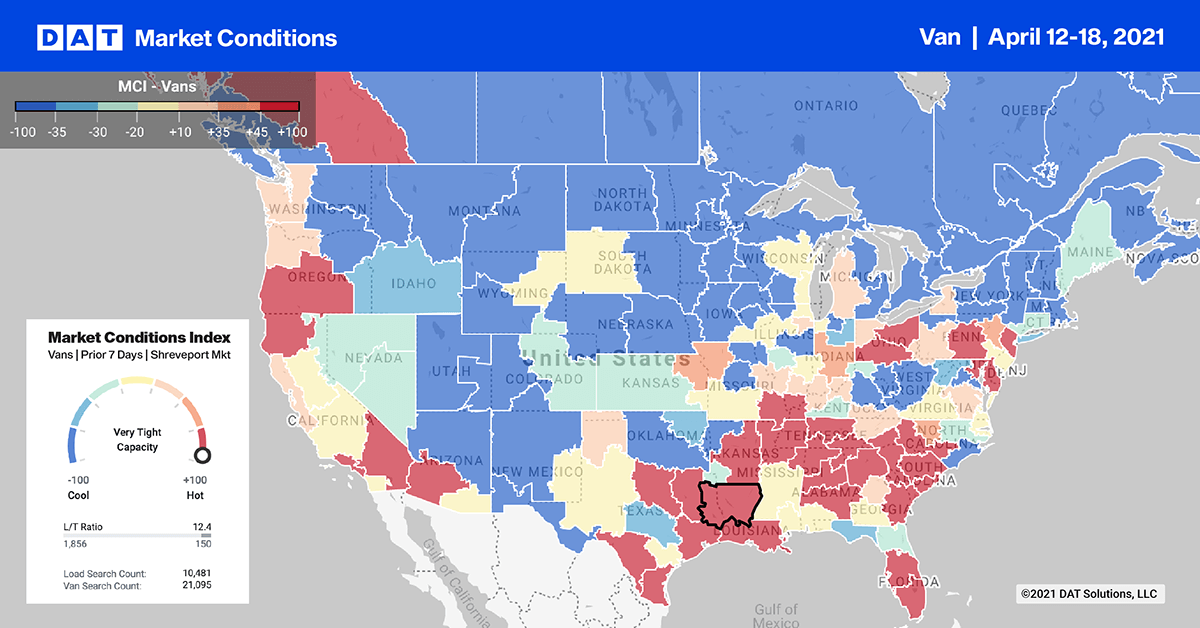

Average spot rates in the top 10 markets dropped $0.03/mile followed by a 5% week-over-week decrease in load post volumes. The average rate was $2.49/mile last week, which was $0.16/mile higher than the national average for all 135 markets.

- Atlanta’s (#1) load post volumes dropped 7% w/w and capacity loosened with rates dropping $0.04/mile to $2.38/mile

- Ontario’s (#4) volume increased by just 1% w/w and capacity tightened with rates increasing $0.02/mile to $3.02/mile

- L.A.’s (#6) volume dropped by just 1% and rates stayed at $2.91/mile