Steel output in the U.S. in the week ending April 23 fell by 2.7% compared with the same time frame in 2021, according to the American Iron and Steel Institute (AISI). Domestic raw steel production was 1,784,000 net tons while the capability utilization rate was 81.7% compared to 1,834,000 net tons a year earlier. Adjusted year-to-date (YTD) production was 28,200,000 net tons, at a capability utilization rate of 80.3%, which is down 1.1% from the 28,506,000 net tons during the same period last year. In flatbed truckload equivalent terms, that’s roughly 12,240 fewer truckloads of steel so far this year.

Even though YTD volumes are down, weekly volumes were up 1% w/w or about 720 more truckload equivalents with the largest regional gains recorded in the Southern Region (43% of weekly tonnage) where volumes increased 2.1% w/w from 750,000 to 766,000 tons. That’s the equivalent of an additional 640 weekly truckloads. The second largest region is the Great Lakes (32%) where production increased 1.6% w/w or an additional 360 truckload equivalents.

In Gary, IN, the largest steel-producing freight market, load post volumes increased slightly by 4% w/w after four weeks of declining volumes. Outbound spot rates remained flat at an average of $3.96/mile excl. FSC but tightened on the 445-mile haul west to Minneapolis, where spot rates were up $0.05/mile to $4.38/mile excl. FSC this week. Spot rates were identical on the short-haul run south to Columbus, O.H., while they remained flat at $3.18/mile excl. FSC on the run west to Oklahoma City.

Flatbed capacity continues to tighten in the Houston market, where spot rates increased another $0.05/mile last week to an average outbound rate of $3.08/mile excl. FSC. On the number one lane north to Fort Worth, however, loads moved dropped by just over 3% last week and spot rates plunged by $0.50/mile below the April average to $3.28/mile excl. FSC but up by the same amount compared to the previous year.

Flatbed capacity tightened on the West Coast in the Ontario freight market following an 11% w/w increase in load post volumes last week. Average outbound spot rates jumped by $0.17/mile to an average of $2.90/mile excl. FSC. Rates for loads to Salt Lake City increased by $0.05/mile to an average of $3.38/mile excl. FSC or around $0.20/mile higher than the previous year.

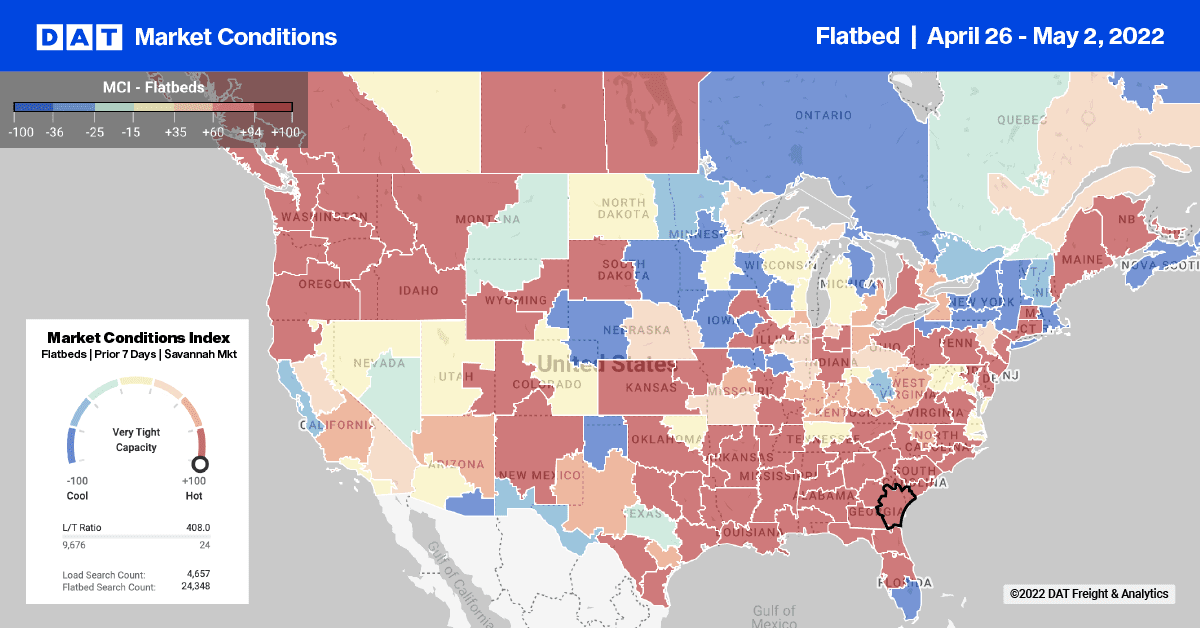

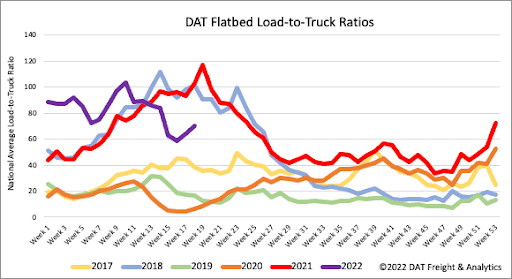

Flatbed load post volumes increased by 5% last week but remaine down 11% m/m and 14% compared to last year. Carrier equipment posts decreased by 4% last week, resulting in the flatbed load-to-truck (LTR) ratio increasing by 9% w/w from 64.03 to 70.02. Separating out the LTR components, load post volumes are very close to 2018 levels while equipment posts are close to 2017 levels.

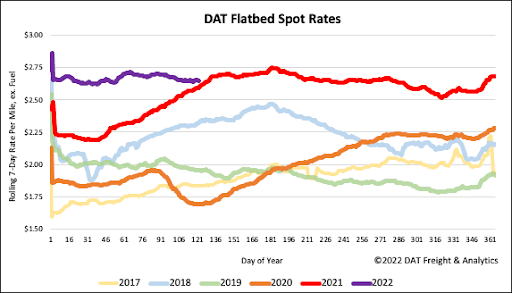

After getting close to the record-high of $2.75/mile excl. FSC on Independence Day last year, flatbed rates retreated again last week, dropping by $0.02/mile, making it three weeks of successive declines. Last week’s national average was $2.67/mile excl. FSC is $0.06/mile higher than the previous year and $0.33/mile higher than the same week during the 2018 flatbed rate rally.