The U.S. is the world’s largest turkey producer and exporter of turkey products by far, accounting for 52% of global production, followed by Germany and Brazil with 10% each. But all is not well in the U.S. domestic market this year, and there’s a good chance frozen and fresh turkeys will be in tight supply this Thanksgiving. Expect to pay more at the very least. According to IRI, traditional Thanksgiving meals are estimated to cost 13.5% more than they did a year ago.

We’ll be seeing fewer turkeys again this Thanksgiving.

According to the Animal and Plant Health Inspection Service (APHIS) of the US Department of Agriculture, since February, a viscous and enduring strain of the highly pathogenic avian influenza (HPAI) virus has devastated nearly 250 commercial flocks and close to 300 backyard flocks. This has resulted in the destruction of over 47 million birds. Market analysts wonder if this year’s Thanksgiving table will be able to feature the holiday’s favorite protein centerpiece. At the same time, some industry insiders say there’s no need to worry, but some preparation might be necessary.

According to Beth Breeding, spokesperson for the National Turkey Federation (NTF), “Consumers wanting to purchase a frozen turkey will be able to find one, but if consumers were hoping to purchase a non-frozen product, then we do encourage them to shop early, plan ahead, check with retailers and get on a waiting list.”

Which states produce the most turkeys?

Remember to be thankful for Minnesota, The Land of a Thousand Lakes, when you sit down to Thanksgiving dinner this year. Minnesota is the number-one state for turkey production by a wide margin. So it’s no big surprise that the Minneapolis market area will also be the land of a thousand loads per day this Thanksgiving as fresh turkeys are stuffed into reefers.

According to the USDA, the number of turkeys raised in the United States during 2022 is forecasted at 212 million, down 2% from the number raised in 2021. Minnesota’s largest turkey-producing state is 37.5 million turkeys, down 7% from the previous year. North Carolina produced 28.0 million turkeys, also down 7%, while Arkansas produced 27.0 million turkeys, unchanged from last year. Indiana produced 20.5 million turkeys, also unchanged from last year, while Missouri produced 17.5 million turkeys, up 3% from last year.

Domestically, turkey production is scattered, with 174 plants located in 20 states. The following five states account for 58% of production:

- Minnesota

- North Carolina

- Arkansas

- Indiana

- Missouri

According to USDA data, these top five states produce around 130 million live turkeys at an average live weight of 30.57 pounds. Most production plants are located within 100 miles of farms. Because of the regional location of farms and processing plants close to feeding sources, the outbound truckload freight task typically involves a much longer length of haul, given the distance to distribution centers located close to major consumer markets.

Minnesota consistently ranks first in U.S. turkey production and includes both the Minneapolis and St. Cloud freight markets, with St. Cloud, MN, roughly at the center of turkey farming activity — or locally known as the “turkey belt.”

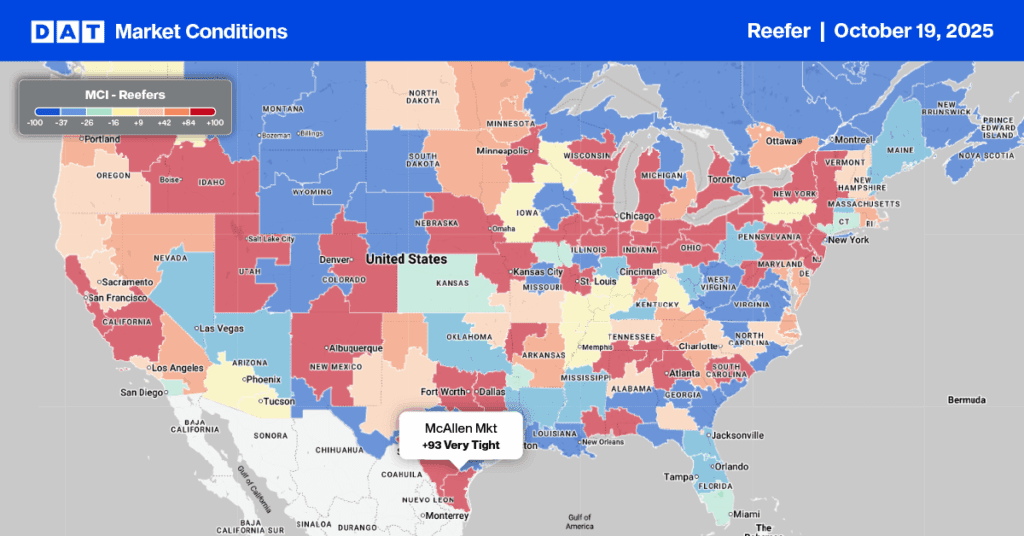

Which turkey markets are hot, and which ones are cold?

Reefer loads out of Minnesota are up 3% or .09/mile compared to last week. Spot rates are steady this week at an average outbound rate of $2.65/mile. Spot rates from St. Cloud to Columbus, OH, are up $0.24/mile to $2.82/mile compared with last month’s average. Loads from Minneapolis to Atlanta, GA, are $3.03/mile, which is $0.11/mile higher than the previous month’s average. However, rates from Minneapolis to Los Angeles declined to $1.84/mile, down $0.15/mile from the prior month.

Overall rates for the second-largest turkey market, North Carolina, were down $0.01.mile w/w. However, Greensboro to Harrisburg, PA, has seen a m/m increase of $0.48/mile, averaging at $3.03/mile.

In other parts of the country, reefer rates were up 4% or $0.12/mile in Ohio, a critical state for distribution centers. The spot rate from Columbus to Charlotte, NC, jumped w/w by $0.39/mile to $3.62/mile. Cleveland to Harrisburg, PA, had high volumes last week, and rates were up $0.12/mile at $4.19/mile.

Reefer rates out of Illinois also had a surge last week, with volume to Ohio being one of the primary factors. Joliet, IL, to Columbus, OH, averages $4.48/mile, which is $0.53/mile higher than the October average. Rates from Joliet, IL, to Cincinnati, OH, are also up, averaging $4.84/mile and $0.79/mile higher than October’s average.

Reefer rates for South Carolina increased by 14% w/w, with loads to Florida being a key driver. Loads from Columbia, SC, to Lakeland, FL, averaged $3.13/mile, up $0.18 from the prior week. Nevada was a hot reefer market last week, with rates averaging $0.07/ mile higher than the national average of $2.83/mile. The main driver of the demand was the short haul lane of Reno to Fresno, where rates are up $0.67/mile at $3.33/mile.