A few weeks ago, we were predicting that there would be a surge of freight availability on the spot market, possibly leading to third peak in October. With one week left to go, October volume remains robust, but a nationwide surge is not forthcoming. Instead, we are seeing some distinct pockets of opportunity, accompanied by strong spot market rates across the country.

Rates have remained surprisingly stable for many months. The national average for vans has hovered above the $2.00-per-mile mark for most of this year, even as fuel prices decline steadily. Fuel is a major cost component for trucking operations, along with labor the payments on the truck itself. You would ordinarily expect rates to drift down as fuel becomes cheaper and seasonal demand softens.

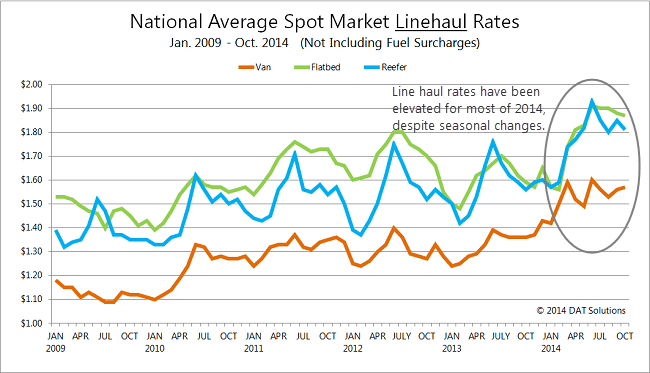

Since July, reefer and flatbed rates have mostly been dropping, as is expected with the change in seasons. Van rates are not. Even as fuel prices decline, leading to a drop the related surcharges that are folded into spot market rates. Average fuel surcharges have fallen below 50¢ per mile for all equipment types, but the line haul portion of the rate is rising, and the total rate per mile is unusually stable.

Linehaul rates have been elevated throughout much of 2014, contributing to rate stability as fuel costs and surcharges decline.