We’re entering another unusual stage in the freight market as the market bounces along the bottom of a trough. The challenge is we may be here for some time to come. Not only are truckload carriers aggressively calibrating truck counts to match softening demand, but they’re also ordering more new trucks from factories ahead of the 2027 EPA Clean Trucks Plan, which could add as much as $30,000 to the cost of new trucks.

The flow-on effect is more used trucks hitting the market and lower used truck prices, making it attractive for new capacity to enter the market when it is already oversupplied. The 2027 pre-buy cannot be ignored, as it’s one of the main reasons we think capacity will keep a lid on any meaningful improvement in spot and contract rates this year.

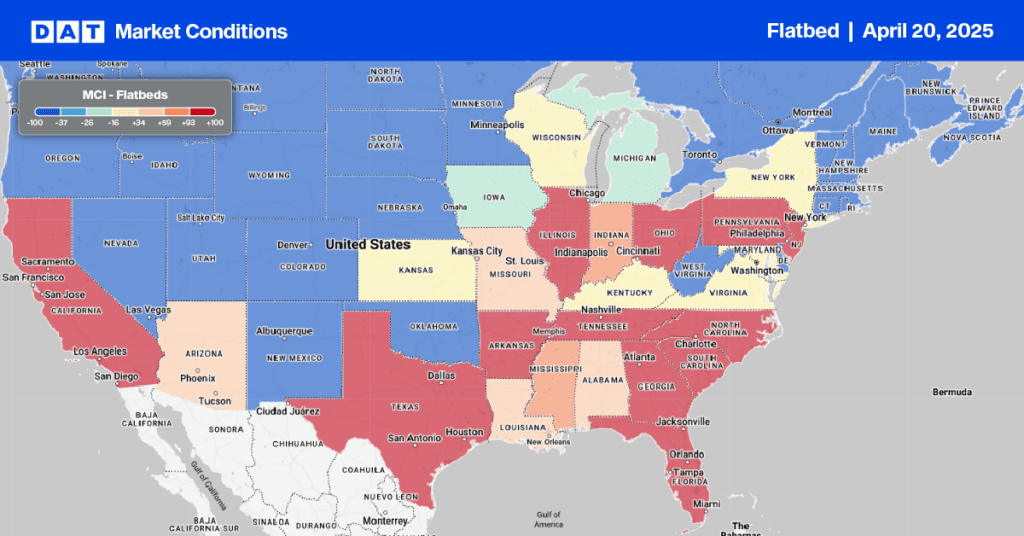

To gauge how much carrier capacity has left the market, the Journal of Commerce Truckload Carrier Index provides insight into how large fleets have yet to reach their collective target, even after cutting truck counts for the past seven consecutive quarters.

According to Bill Cassidy at the Journal of Commerce, “big carrier capacity cuts in the first quarter pulled the Truckload Capacity Index (TCI) down to levels last seen in mid-2017. The TCI dropped 2.4% from the fourth quarter to a first-quarter reading of 78.9. The index fell 7.7% from Q1 2023.”

The TCI, a measure of capacity at large publicly owned carriers based on end-of-quarter truck counts, has fallen precipitously over the past two years after reaching a high point of 93.2 in the second quarter of 2022. The last time the TCI was below 80 was in the third quarter of 2017 — before the capacity crunch and trucking boom of 2018.

Since the TCI peaked in 2022, the publicly owned carriers in the index survey group have cut their collective truck count by 15.4%. The index drop of 14.3 percentage points in 2022–2024 is the largest since a 26.2 percent drop from 2007 through 2013.

During an April first-quarter earnings call, David Parker, chairman and CEO of Covenant Logistics, told analysts, “We just continue to bounce on the bottom. The million-dollar question is when will enough capacity exit (finally tighten the market and push up pricing).” Covenant was the only company in the Journal of Commerce TCI group to increase its truck count yearly by 99 trucks, although it cut ten trucks from its fleet sequentially from quarter to quarter.

Knight-Swift Transportation Holdings, which owns three of the largest US truckload carriers, told Wall Street analysts, “We have lost contractual volumes because we were not willing to commit to further concessions on what we view as unsustainable contractual rates,” Brad Stewart, Knight-Swift’s treasurer and vice president of investor relations, said “ This resulted in more of our capacity being allocated to the spot market, which creates further pressure on revenue per mile and utilization in the near term, but positions capacity to react to changes in the market when the market does inflect.”

Absent any meaningful change in freight demand, 2024 is shaping up a lot like last year and 2019, which were poor years for transport providers but good years for shippers.